If you’re a business owner with less-than-perfect credit, you might feel like your funding options are limited — or even nonexistent. Traditional banks often turn away small businesses with poor credit scores, making it challenging to get the working capital you need to grow.

But here’s some good news: there are funding solutions that don’t rely on your personal or business credit score — and invoice factoring is one of the most flexible options available.

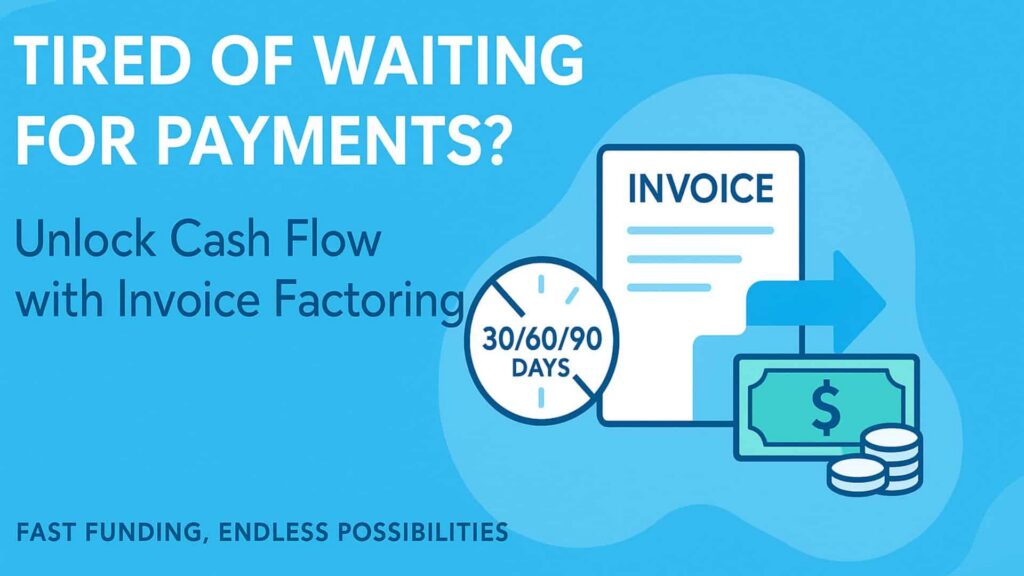

What is Invoice Factoring?

Invoice factoring is a form of alternative business funding that helps companies improve cash flow by turning unpaid invoices into immediate working capital.

Here’s how it works:

- You deliver your product or service to your customer as usual and issue an invoice.

- Instead of waiting 30, 60, or even 90 days for payment, you sell that invoice to a factoring company.

- The factoring company pays you a large percentage of the invoice upfront — often within 24 hours.

- When your customer pays the invoice, the factoring company sends you the remaining balance, minus a small fee.

Why Credit Doesn’t Matter with Factoring

Unlike traditional loans, invoice factoring doesn’t depend on your credit score. That’s because factoring companies are more interested in the creditworthiness of your customers — the ones who owe you money.

If your customers have a strong payment history and good credit, you can get funded even if your own credit is poor.

Who Can Benefit from Factoring?

Factoring is especially helpful for businesses that:

Have slow-paying customers (typical in industries like staffing, transportation, manufacturing, or business services)

Need cash flow to cover payroll, rent, or new projects

Have been turned down for a traditional bank loan due to low credit

Want to grow without taking on debt

The Bottom Line

If you’ve been asking, “Can I get funding with poor credit?” — the answer is YES. With invoice factoring, your business’s credit score isn’t the roadblock it might be elsewhere.

At AFS, we make it simple to unlock the money tied up in your outstanding invoices — no personal credit check required.

Ready to find out if factoring is right for your business? Contact us today to learn more and get a free quote!

Additional FAQs

- Question: What is the fastest way to get business funding with poor credit?

Answer: The fastest options include invoice factoring or merchant cash advances, which rely on your customers’ invoices or future sales rather than your credit score. - Question: Can startups with no credit history get funding?

Answer: Yes, some alternative lenders and factoring companies approve startups based on cash flow projections, contracts, or customer invoices instead of credit history. - Question: How does invoice factoring help businesses with bad credit?

Answer: Factoring converts unpaid invoices into immediate cash, allowing businesses with poor credit to improve cash flow without taking on new debt. - Question: Are there lenders that specialize in poor credit funding?

Answer: Yes, many online and alternative lenders focus on businesses with low credit scores and evaluate funding eligibility based on revenue and payment history. - Question: What should I look for when choosing a funding option with poor credit?

Answer: Look for flexibility, transparent fees, speed of funding, and lenders who consider factors beyond credit score, such as cash flow and customer reliability.